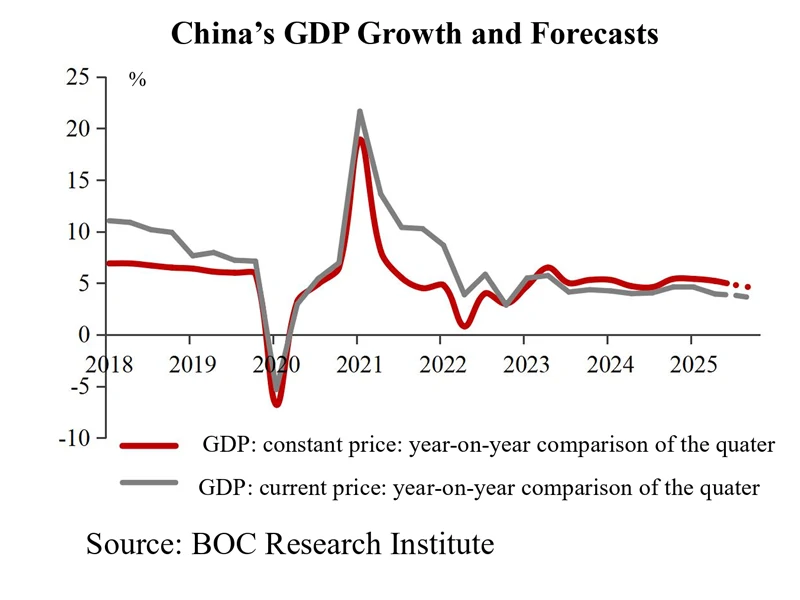

Since the third quarter of 2025, China’s economic growth momentum has moderated. External demand has exceeded expectations, while domestic demand has continued to soften amid the ongoing transition between old and new growth drivers. Preliminary estimates suggest that GDP expanded by around 4.8% in the third quarter, representing a deceleration of approximately 0.5 percentage points compared with the first half of the year.

In the fourth quarter, the external environment remains fraught with uncertainties. Under the disruption of the U.S. reciprocal tariff policies, China’s export growth is expected to moderate. With the diminishing effects of earlier policy stimulus and insufficient endogenous momentum, consumption growth is likely to ease slightly. The drag from the property sector is expected to deepen further. Overall, GDP is projected to expand by around 4.5% in the fourth quarter, bringing full-year growth to approximately 5%.

China is likely to achieve annual growth target set at the beginning of 2025, although downward pressures on the economy have intensified markedly in the second half of the year. Going forward, macroeconomic policy should place greater emphasis on positive incentives and the role of expectation management and stabilization. More attention should be given to the driving effect of demand—particularly consumption demand—on growth, as well as to the marginal effectiveness of macro policies. A well-coordinated policy mix, or “policy toolkit,” should be fully leveraged to mitigate future uncertainties and sustain economic stability.